Example of a Traditional LTC Policy Quote:

Based on a 500,000 pool of money for a maximum monthly benefit of $10,000 per month for 50 months,

Example IUl with “No Discount Formula” Pays benefits dollar for dollar based on the death benefit!

Based on a 500,000 pool of money (Death Benefit) for a maximum monthly benefit of $10,000 per month for 50 months,

LTC Premiums with an 1% average annual rate increase

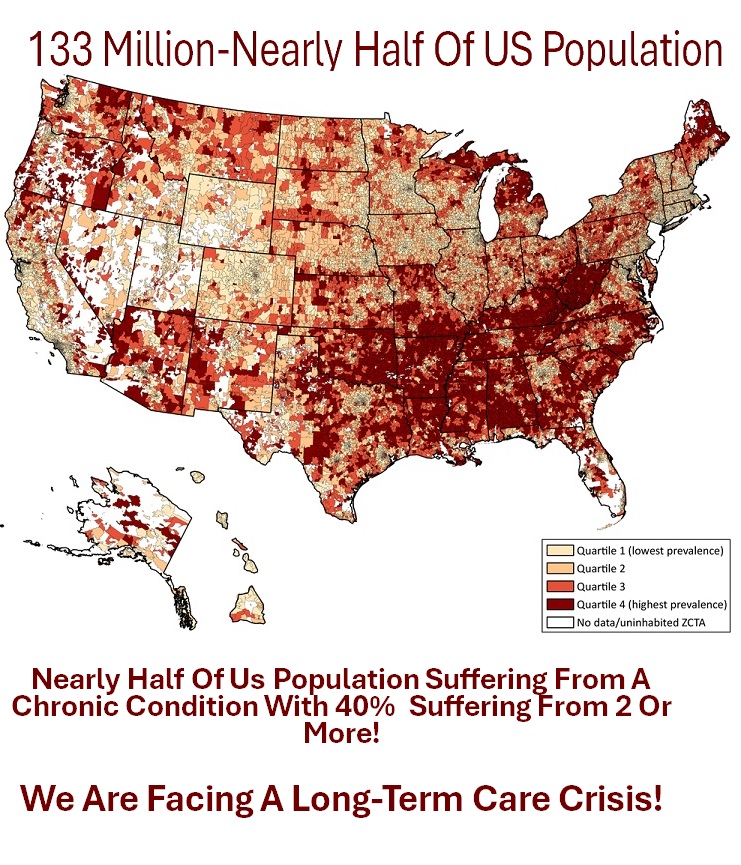

Nearly half the U.S. population—or 133 million Americans—lives with at least one chronic condition, with 40% suffering

from two or more

LTC 8k month 400k 50 months

165.33 60 years 119,037.60

366.04 30 years 131,774.40

LTC 10k month 500k 50 months

139.75 60 years 100,620 (S)

457.55 30 years 164,718.55 per

NET WORTH

Median family net worth

INCOME

Median household income

SAVINGS AND INVESTMENTS

Total savings/investments, workers age 45 to 54

Total savings/investments, workers age 55 +

Case Study: Why Long-Term Care Planning Starts Today!

(In your late 20s & early 30s Don't wait until your 60s)

According to LTC Consumer, along with AARP and others..... by 2055, 3 years long long-term care services will cost $770,778 https://ltcconsumer.com/ltc-facts/statistics/

If you are currently 50 years old expect to pay 3/4 of a million dollars for LTC services!

Are you prepared?***

FACT:

The majority of Americans will not reach retirement having achieved the ability to self-insure from life insurance! This is why 57% of current boomers age (60 to 78) own life insurance, with millions more still in need of life insurance but can't qualify due to age, health and cost!

https://www.bankrate.com/insurance/life-insurance/life-insurance-statistics/#life-insurance-statistics-by-age

Question? If the majority can't self-insure from life insurance, how in the world will you self-insure from life insurance and self-insure from long-term care insurance, both at the same time?

The movie "Mission Impossible" comes to mind...if you choose to accept!

This next part is specially reserved for the BTID crowd! (Buy Term & Invest The Rest)

Overall, this is a failed strategy! It requires everything in your life to work out perfectly.... it's a paper tiger strategy!

I have a few interesting statistics to help prove my point!

For workers aged 55 and older, average retirement savings, including 401(k) and IRA balances, typically range from $244,750 to $426,000, but median balances are significantly lower, around $87,571 to $200,000. Averages can be skewed by high earners, making median figures a more realistic representation of typical savings.

Average and Median Retirement Savings for Workers 55+:

Ages 55-64: Average 401(k) balance is $244,750, with a median of $87,571.

Ages 65-74: Average 401(k) balance is $272,588, with a median of $88,488.

Ages 55-64: According to Kiplinger, the median retirement savings are $185,000.

Ages 65-74: According to Kiplinger, the median retirement savings are $200,000.

Ages 55-59: According to Synchrony, the average retirement savings are $223,493.56.

Ages 60-64: According to Synchrony, the average retirement savings are $221,451.67.

Ages 55-64: According to NerdWallet, the median retirement savings are $185,000.

Ages 65-74: According to NerdWallet, the median retirement savings are $200,000.

If your plan is to leave your family an inheritance and your goal is to become self-insured by the time you retire.....This means you have to save enough money to retire on, and save enough money to replace the life insurance as your inheritance tool!

According to ACLI 2024 Life Insurers Fact Book....The average size of new individual life insurance policies purchased in 2023 was $206,000. https://impact.acli.com/impact-facts-life-insurance-in-force-2/

Assuming you want to at least leave $200,000 as an inheritance or as a way of replacing your income for 1 to 4 years. This amount would wipe out your total retirement savings for the majority of Americans!

The current US average savings isn't enough to fund a 20 to 30-year retirement and leave you with enough to provide an inheritance or life support income to your surviving family!

The numbers prove BTID - Buy Term & Invest The Difference doesn't work for the majority of Americans, no matter how good it sounds!

A study put out by Allianz found:

Inflation, market volatility and recurring financial crises are making planning for retirement even more challenging!

Key findings:

56% consider “financial crises” as a permanent part of their retirement planning

46% were forced to reduce or stop saving for retirement, and say they won’t be able to ramp up saving any time soon.

53% of Americans are hesitant to invest any additional money in the market for the foreseeable future

Nearly 40% of Americans admit their retirement strategy is derailed and they aren’t sure when or how they’ll get it back on track.

https://www.allianzlife.com/about/newsroom/2023-Press-Releases/Americans-Facing-a-New-Retirement-Reality

This sums up my BTID-Buy Term & Invest The Difference - Paper Tiger Strategy Comment!

It's called "Life Happens"!

Life isn't perfect so your financial roadmap should account for when life throws a bunch of curveballs at you!

For the majority of Americans, it's literally mission impossible for you to become self-insured for both life insurance and long-term care without having to dip into your retirement income nest egg!

The next time someone says Buy Term & Invest the Difference to you!

Kindly ask them to view their book of clients who are on pace to have a separate fund of money to replace their life insurance needs, along with another separate fund of money to replace their long-term care needs, along with a separate fund of money for income during retirement!

Since the majority of Americans earn under $80,000 per year (single)....Make sure they show you their clients, only using average and median income ranges!

Until I see the average and median retirement nest eggs with enough money to account for a life insurance inheritance along with monies for long-term care services without having to dip into your retirement income.... I will stand by my statement that BTID -Buy Term & Invest The Difference" doesn't work for the majority of Americans!

BTID Rant Over: Next!***

If you follow famous radio/podcast/tv financial gurus..... Because of cost, many suggest waiting until age 60 before purchasing a Traditional Long Term Care Policy; however, this is terrible financial advice!

The problem is this:

In 2021 according to the American Association for Long-Term Care Insurance...

A whopping 30.4% of individuals age 60-64 were declined a long-term care policy!

That's 30 out of 100!

A whopping 38.2% of individuals age 65-69 were declined a long-term care policy!

A whopping 47.2% of individuals age 70-74 were declined a long-term care policy!

***

A few examples of diagnosed health conditions that may disqualify you for long-term care insurance include (but are not limited to):

Alzheimer’s disease or other forms of dementia

Parkinson’s disease

Amyotrophic lateral sclerosis (ALS)

Cerebral palsy

Multiple sclerosis (MS)

Kidney failure

Obesity

Hypertension (high blood pressure)

Sickle cell anemia

Cardiomyopathy

AIDS or HIV infection

Stroke or history of transient ischemic attacks (TIAs)

Cancer (depending on the type, stage, and treatment history)

Spinal cord injury

Chronic illnesses like advanced diabetes or severe arthritis

Having more than one Chronic illness

Hip replacement

Knee replacement

Waiting until you turn 60 or entering your 50s to tackle the long-term care issue....is not the best retirement-friendly strategy.

With America's health crisis, these numbers stand to get worse!

Nearly half the U.S. population—or 133 million Americans—lives with at least one chronic condition, with 42% suffering from two or more chronic illnesses and 12% have at least 5 chronic illnesses....According to cds. gov and aha .org

This figure is 15 million higher than just a decade ago, and by 2030, this number is expected to reach 170 million.

https://www.cdc.gov/pcd/issues/2024/23_0267.htm

https://www.aha.org/system/files/content/00-10/071204_H4L_FocusonWellness.pdf

Long Term Care Insurance is very expensive....I get it!

Studies show that the high cost of LTC premiums, along with increasing premiums, prevent many seniors from getting and keeping an LTC plan.

Currently, 70% of current 60-year-olds will need LTC services; however,.....

Currently, only 14% of current retirees have an LTC plan in place.(Yikes)

https://acl.gov/ltc/basic-needs/how-much-care-will-you-need

LongTermCare.gov

We are on the verge of a major long-term care crisis!

According to "LTC Consumer"...… $770,778 is the projected average cost for 3 years of long-term care 30 years from now!

https://ltcconsumer.com/ltc-facts/statistics/

If you are 50 today and end up needing long-term care services in your 80s, you could be faced with a $770,000 price tag, a price that could jeopardize or wipe out your remaining retirement nest egg for the surviving spouse or for both and wipe out any inheritance you wanted to leave behind!

Women face the largest burden of caring for a husband needing long-term care!

According to studies, women tend to live longer, often face difficult financial obstacles after surviving a spouse who required long-term care services.

The overload of reports and studies seems to suggest that waiting until the 50s or 60s before putting an LTC plan in place is a terrible financial move!

70% of current 60-year-olds and 77% of current retirees will need long-term care services; however, only 14% of current retirees have a plan in place!

It's about the money!

Long-term care premiums are not cheap!

1. Most long-term care premiums increase over time. If retired and on a fixed income....who wants to pay for a product with increasing premiums?

2. Waiting until you are older is a terrible strategy. Most think about purchasing LTC during a time when they are least likely to qualify for a decent plan as a result of being older with health conditions!

3. If you spend $170k plus on long-term care premiums during retirement and you die without accessing any of the long-term care benefits.... your beneficiaries get nothing, Zip Nada, Zilch!

(NOTE: There are LTC plans that provide for a return of premium; however, if the base LTC policy is too expensive for the majority...how can you afford a return of premium feature? Adding a return of premium rider is certainly cost-prohibitive.)

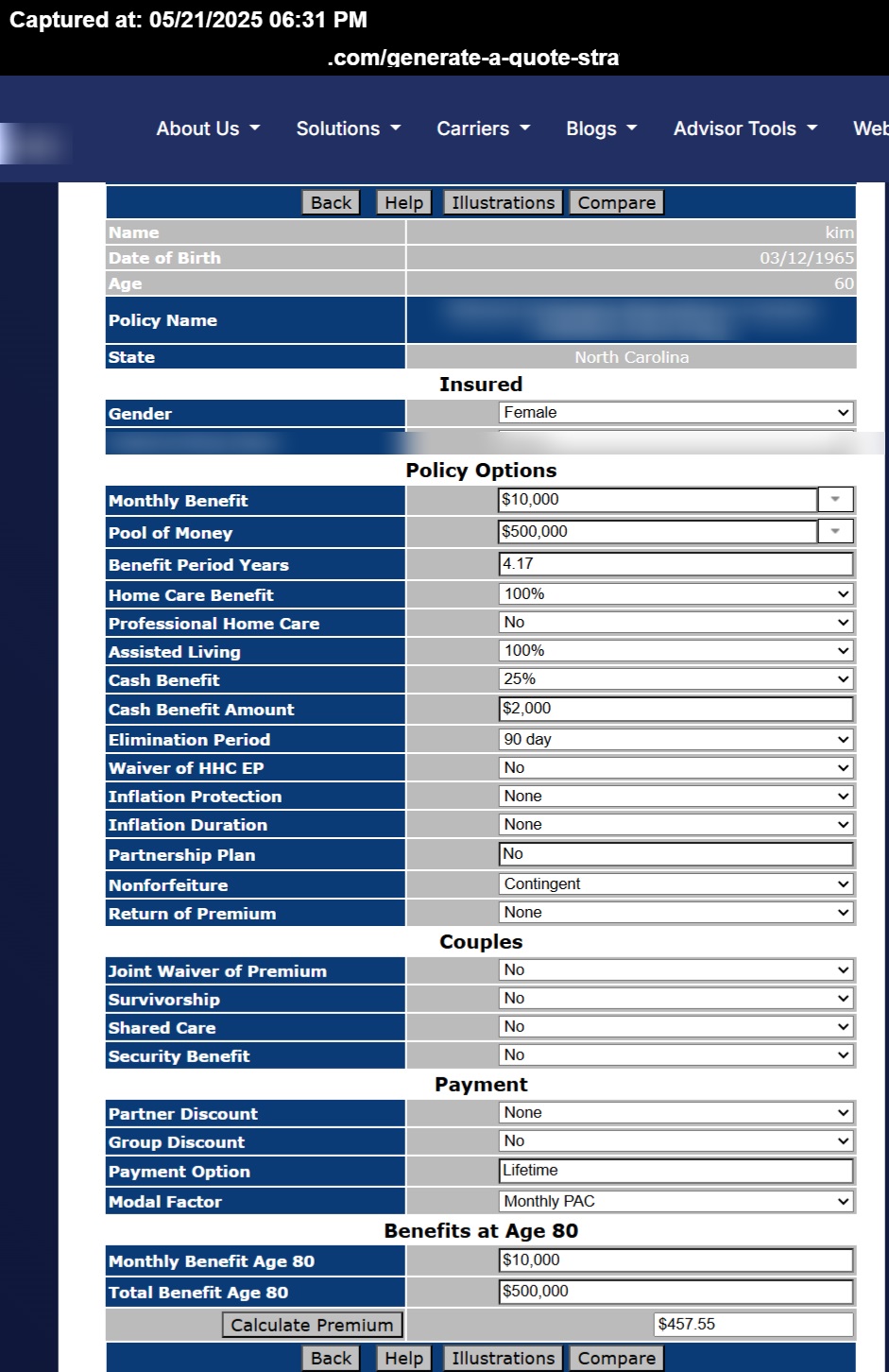

A long-term care policy with a pool of money for a female age 60 without return of premium is: $457.55 per month. With a return of premium the cost balloons to $662 monthly!

Most individuals who start off with a return of premium LTC policy drop the return of premium rider after their first premium increase! Why bother?

I referenced increasing long-term care premiums earlier and not to add insult to injury but according to Milliman. com.

In 2024 Insurers requested an average rate increase of 56%, according to the 2024 Milliman survey reported on 14 April 2025

The average rate increase that was approved was *28%*

https://www.milliman.com/en/insight/ltc-rate-increase-landscape-update

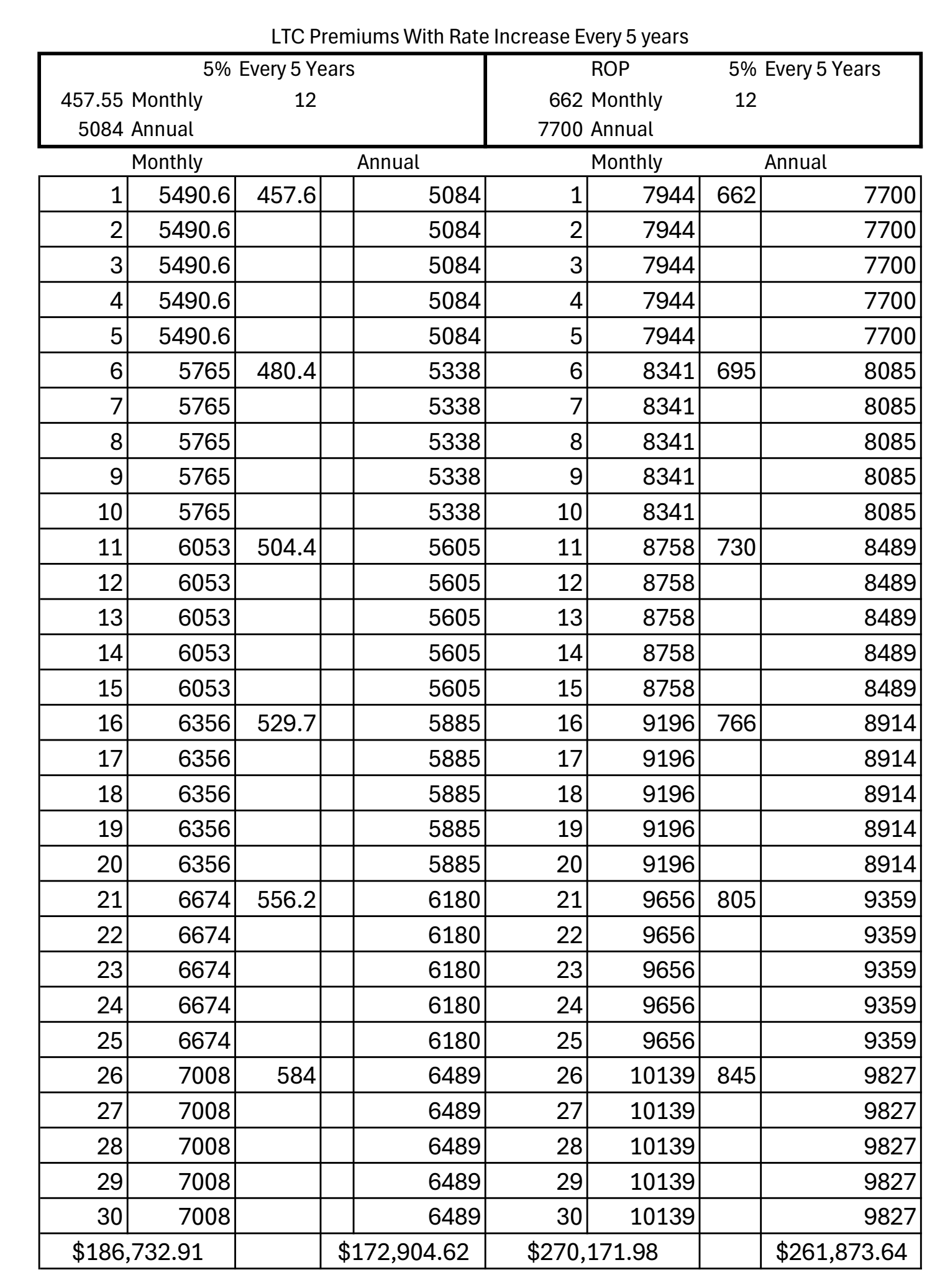

Imagine paying $457.55 for a long-term care policy providing $10k per month in benefits with a money pool of $500,000 and you receive a notice in the mail increasing your premiums to $480.404 per month! Then....Imagine receiving another premium increase to $504.40 a few years after the 1st increase! Another increase 5 years later to $529.70 per month.... another increase to $556.20 and as your retirement years are winding down a final increase to $584 per month. (These increases represent a below normal rate increase of 5% every 5 years, covering a 30-year retirement) Note: Just last year (2024), insurers requested a 58% increase and got approved for a 28% increase but I only used 5% in my example! What will the rate increase request be this year for 2025?

Based on the numbers and not based on opinions.... Traditional long-term care plans are not solving the long-term Care Crisis! Americans as a whole can't afford them, and can't afford to self-insure for long-term care either!

The solution I'm about to recommend is not for everyone, but can certainly help the majority! There is no one-size-fits-all! For some, a traditional long-term care policy will be the best option. For some, using an annuity with an LTC provision will be the best option. For some, using a life insurance policy set up with guaranteed premiums that includes benefits for LTC-type services will be the best option. For individuals with a whole life or any cash value life policy that doesn't have LTC type benefits, you can use the cash value inside of the policy as a free 1035 exchange into an annuity with LTC benefits. For some, selling your cash value life insurance policy to a 3rd party will be the best option! For some, using a long-term care benefit plan that converts life insurance into monthly payments will be the best option. (Many attorney estate planners use the LTC Benefit Plan option and the hybrid life insurance option for LTC purposes)

When proper planning doesn't happen a few of these strategies I mentioned could help out!

I'm in favor of using your life insurance policy as a triple + 1 protection asset to help protect against premature death during your working years, medical foreclosure due to suffering a critical illness such as a heart attack, cancer or stroke during your working years into pre retirement years along with helping to protect against the cost of long term care premiums and long term care services...The "Plus 1" I referenced, I'll get to in a few minutes. This strategy is my alternative to traditional long-term care insurance!

***Not everyone, but many people can benefit from using an alternative to traditional long-term care insurance!

Planning ahead is required!

My alternative to traditional long-term care is to use an IUL - Index Universal Life policy with living benefits set up with ENLG -Extended No Lapse Guarantee Premiums!

Most of the time, when you think of "IUL" the cash value component is all you hear people talk about! (Good or Bad)

However, when used in part as an alternative to traditional long-term care insurance, the cash value built up doesn't matter.

With this strategy, you are not setting the policy up to access cash value today or in the future. You will not access the cash value with this setup! The cash value can show ZERO every year with this design. The cash value is of little importance when the IUL is set up with the ENLG -Extended No Lapse Guarantee Premium.

An IUL with the ENLG -Extended No Lapse Guarantee Premium option will guarantee your premiums and death benefit will stay the same for the entire ENLG period regardless of the cash value growth, regardless of your rate of return, regardless of the rising cost of insurance or ARTs....as long as you don't touch the policy and all you do is make your on time premium payments!

I must warn you! Individuals who are anti-IULs but claim to be expert IUL reviewers don't understand how the ENLG premiums work when looking at the illustration.

In part, it's because they are viewing a cash value policy and in their mind they think all cash value polices are supposed to build cash value, and if they don't, there's something wrong with the policy lol.

They will look at the policy and show you the zeros in the cash value column, and will wrongly tell you the policy is going to lapse when you see zeros in the cash value column.

This is False!

When you see a zero in the cash value column in the same year, you see a zero in the death benefit column.... This is when the policy will end.

To be clear! If you purchased a cash value policy with the purpose of only growing cash value and you see a bunch of zeros in the cash value column...Well, this is a problem!

If you see a bunch of zeros in the non-guarantee column in the early years....this is your first clue that the policy wasn't set up for cash value. Another clue is when you have an "even" number as the death benefit! This is the 2nd clue that the policy wasn't set up for cash value.

When setting the policy up for just the death benefit...in the software you say...ok show me how much a 500,000 policy costs and the software will give you a premium amount.

When setting the policy up with the purpose of building maximum cash value, it works the opposite!

With the software, you say...ok show me the minimum death benefit based on only paying whatever amount you want to pay... let's say $500 per month. It's virtually impossible for the software to return an even death benefit number when you ask it to solve for the minimum death in connection with the money you want to pay!

With the death benefit option $150 per month might buy you $500,000 in death benefit but with the second option, the same premium of $150 set up for cash value might only buy you $87,452 in death benefit!

With both options, you are paying the same amount of premium dollars but as a result of paying for more life insurance death benefit with the $500,000 option, you will grow very little cash value as the majority of your premiums are paying for the cost of insurance! With the 2nd option, the majority of your premiums are going towards the cash value buckets inside of the policy and as a result, you'll grow significantly more cash value!

Recap: If you have a cash value policy with an even death benefit, such as an even 500,000 this is the first clue it wasn't set up for maximum cash value growth..... this is ok if the cash value growth isn't a priority but instead the death benefit and living benefits is the priority! It's not ok if the cash value is the priority!

With this little educational moment, you are now 10 steps ahead of all the so-called expert IUL reviewers lol!

****

Let's now get back to the IUL set up to have little to zero cash value by using the ENLG -Extended No Lapse Guarantee Premium option with living benefits.

Using an IUL as an alternative to a traditional long-term care policy really only works when using an IUL with predictable premiums that are guaranteed for the term of the IUL.

Different IULs offer different ENLG -Extended No Lapse Guarantee Premium periods.

Some will only guarantee the premium to age 88, a few will guarantee the premium to age 90 a few will guarantee the premiums to age 95 to include every year up to a maximum of age 121!

The guarantee period can be customized to meet your life longevity concerns!

As a rule of thumb, If I'm helping an individual age 40 or higher, I might only set the guarantee period to age 90! If dealing with a 30-year-old the minimum guarantee period I'll use is age 95! If I'm helping someone under the age of 30 to 25 I'll use an IUL with a minimum guarantee to age 105. If under the age of 25 I'll use an IUL with a minimum guarantee extending to age 121!

If you are age 50 and request a minimum guarantee to age 121... that's what you'll get! This isn't a one-size-fits-all all approach!

I mentioned earlier, not all living benefit life insurance polices pay the same!

There are 3 main types of living benefit payouts:

1. Discounted formula

2. Lien formula

3. Dollar Per Dollar Formula

When it comes to using an IUL as an alternative to long-term care insurance.

The IUL "Must" have guaranteed premiums to the age requested.

The IUL "Must" use the Dollar per Dollar living benefit option.

The Lien formula will work as long as the lien is no more than half a percent.

****I never consider an IUL that uses the discounted formula for living benefits!

Discounted formula example:

1. With the discounted formula on a 500,000 policy as the example!

96% of this policy is eligible for acceleration.

20,000 left as a death benefit.

120,000 maximum acceleration each year for 5 years.

Assuming age 80!

Each year in this example, the acceleration is based on 120,000, but only 77% of this amount will be received as a living benefit. The percentage can change it year as you age.

Year 1:$92,409 is the payout after the discounted formula = 77% of the eligible acceleration.

Year 2:$94,089

Year 3:$96,289

Year 4:$99,089

You are accelerating $120,000 each year, but after the discount, you'll receive a lower amount.

For this example:

Total payout $381,876 plus a 20,000 death benefit:

The Acceleration costs you $98,124 on a 500k policy.

This method usually has a lower lifetime premium in exchange for the discounted living benefit formula!

The discounted formula is not calculated until the time you file a claim. 30 years from today, you have no idea what your acceleration could be.

This is why I never use this living benefit structure. Some people will say something is better than nothing!

Wrong answer if using this specifically to help control future long-term care costs.

2. Lien Formula

This method is almost dollar-for-dollar! The IULs I use with this formula charge just under a half percent of he death benefit! This is as close to dollar per dollar as you can get.

3. Dollar Per Dollar Formula!

Example if you have a 500,000 policy, you can accelerate the full 500,000!

Or some companies with dollar per dollar will allow you to accelerate 80% (and allow you to use 100% of the 80% for acceleration, with 20% left as the death benefit.

So on a 500,000 policy, you can accelerate 100% of the 80% death benefit, which is $400,000, with $100,000 left as the death benefit!

With the discounted formula, you lose a portion of the death benefit! With the dollar-for-dollar formula, whatever you don't use for LTC type services, your beneficiaries will get as a death benefit

Its dollar per dollar.

If you use an IUL that allows you to accelerate the entire death benefit amount...using the same 500,000 example and based on a 2% monthly payout! You can accelerate $10,000 per month for 50 months (500,000). You don't have to accelerate the entire 500,000 amount. You could accelerate 10k per month for 45 months, leaving 50k as your death benefit or accelerate $200,000 and you die, leaving $300,000 as a death benefit!

Recap:

Two things you must get right when using an IUL as an alternative to traditional long-term care insurance.

1. The cash value must mean nothing to you because you'll never touch the cash value. The premiums have to be set up at the minimum premium that will guarantee the coverage up to age 121, depending on your life expectancy! As a default, you can simply set it to age 121!

2. Use an IUL with a dollar per dollar living benefit payout with the Lien option as a close 2nd but never use an IUL with the discounted formula!

The trick is finding an IUL with both of these attributes! I have a small list of 10!

The list is long (over 300) with IUL polices offering one or the other...but to have what I consider the main essentials, there are only a few IULs that will work!

Let's look at some numbers.

Example:

A female age 30 in good health can purchase an IUL life insurance policy with living benefits! These living benefits can be used as an alternative to a traditional long-term care policy.

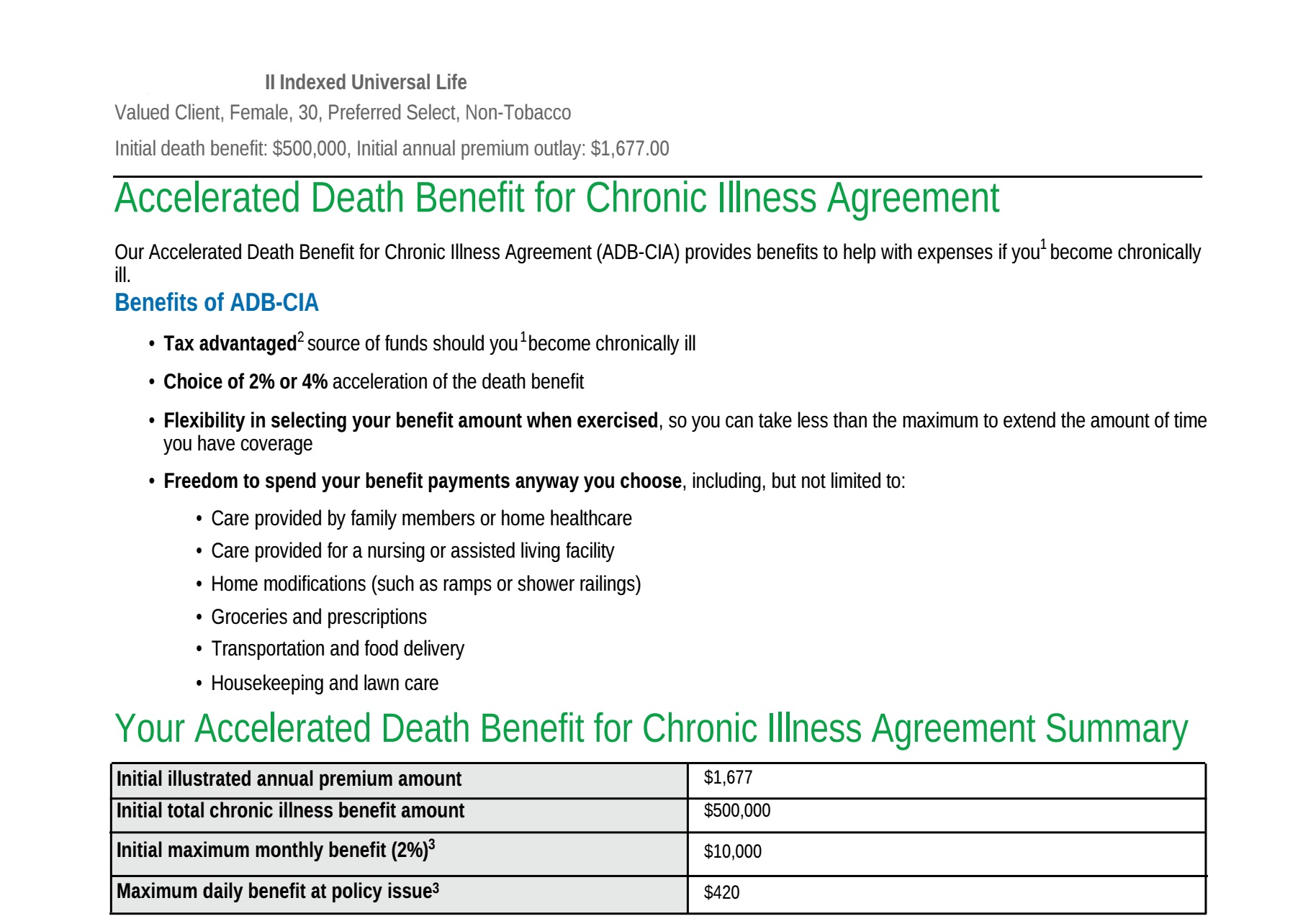

A 500,000 death benefit with a dollar per dollar matching chronic illness benefit or LTC rider that also provides for $10,000 in monthly benefits for 50 months will cost $139.75 per month.

***I would like to reiterate that this particular policy is an IUL -Index Universal Life Insurance policy with a no lapse guarantee/guaranteed premium!***

My preferred recommendation is to start planning for LTC in your late 20s & early 30s

I will compare the cost of purchasing an alternative to LTC (An IUL with living benefits) at age 30 vs waiting to age 60 to purchase a traditional long-term care policy!

Both plans will offer a $10,000 monthly benefit for 50 months! (500,000 total pool of money for LTC type services)

A female age 30 in good health can purchase a $500,000 Living benefits IUL with a No Lapse Guarantee/Guaranteed Premium to age 96 at $139.75 per month.

A female waiting to age 60 purchasing a traditional LTC policy with a $500,000 pool of money providing $10,000 per month in benefits for 50 months will cost $457.55 per month.

The total cost of the IUL in this example from age 30 to age 90 (60 Years) will total $100,620.

The cost of the LTC Policy purchased at age 60 to age 90 (30 Years) will total $164,718.

In this example, the IUL premiums are guaranteed not to increase to age 96; however, the LTC policy premiums are not guaranteed.

Remember....reports show that Insurers requested a 56% rate increase for LTC last year and was approved for 28%

In this example, the LTC premiums paid for 30 years will cost $164,718 without accounting for any rate increase; however, if we account for just a 5% rate increase every 5 years, the total premiums will equal $186,733 in this example.

As you can see with this example:

A female can purchase an IUL with dollar-for-dollar living benefits at age 30 and pay on this policy for 60 years, and pay less than waiting to age 60 and purchasing a traditional LTC policy paying on it for just 30 years....(And that's if you don't get turned down due to health conditions)

The IUL with guaranteed premiums in this example costs $100,620 over 60 years, while the traditional LTC policy with rate increases over 30 years will cost $186,733

If, after paying $186,733 for the traditional long-term care policy, you die without ever needing to use the policy!

Your beneficiaries will get nothing, Zip Nada Zilch!

However....

If after paying $100,620 for the IUL policy with living benefits and you die without ever needing to use any of the living benefits...Your beneficiaries will get a $500,000 death benefit!

This IUL policy is certainly a triple protection plus one product!

(Please Note: I'm not renaming this IUL only speaking to the different protections it can provide! Also, this IUL is not an investment product...it's simply an Index Universal Life Insurance Policy that offers you the ability to earn a rate or return on the cash value using different indices, along with providing benefits for when you die, along with providing benefits for while you are living!)

Let's review the "PLUS 1"

Another nice perk to having a life insurance policy during retirement is the ability to leverage this policy to increase your lifetime Guaranteed Income!

This strategy is only for individuals and couples who'll take a portion of their retirement income by way of an Annuity with "Lifetime Guaranteed Income." This strategy also works if you'll be receiving a Pension from an employer as a "Lifetime Guaranteed Income."

The goal for most is to limit expenses in retirement, including the goal of not having to pay for life insurance!

With this strategy, the cost of your life insurance policy during retirement will have a wash cost effect. As a result of having the policy, you'll be able to potentially increase your lifetime guaranteed income by at least 4x the cost of the policy!

For example: if the policy for both you and your spouse cost a combined $300 per month but you're able to increase your guaranteed lifetime income by $1,200 per month, the cost of the life insurance policy becomes a wash and you will have increased your lifetime guaranteed income by $900 per month after the cost of insurance or $10,800 each year.

Assuming a 30-year retirement, this could provide you with an additional $324,000 in guaranteed income (after the cost of insurance)!

In a few moments, I will provide you with an actual income payout option, but first, let's talk about how this process works!

A cash value life insurance policy is involved in this process however the cash value portion of the policy isn't involved in this process.. This has nothing to do with the cash value in your policy! You will not use one dime of the cash value!

When using a Pension or Annuity for lifetime guaranteed income, normally you are offered two payout options....Single Life with a certain period or a joint life with a certain period.

Statistics show couples select the Joint with life certain payout 97% of the time!

Why?

The joint payout option guarantees a surviving spouse will not outlive their income!

The cost of the joint payout option can reduce the Single Life payout option by as much as $2,500 per month or more, depending on the size of your Annuity!

(Right about now, I hope a light bulb is going off in your head)

Taking a lower Joint Life payout is absolutely worth it in order to ensure your surviving spouse will not run out of money; however, leveraging a life insurance policy with guaranteed premiums for life is a much cheaper way of accomplishing the same goal while at the same time providing you with more guaranteed income.

With the life insurance policy in place on both you and your spouse, you can select the highest payout option for your lifetime guaranteed income.

Assuming a $1 million annuity along with a $500,000 guaranteed premium iul policy that you purchased when you were young, preferably.

The life insurance policy will serve as the guaranteed lifetime income for the surviving spouse instead of selecting the lower joint life payout option.

The beauty of this strategy is, your life insurance policy doesn't have to equal the starting balance of your annuity.

In this example I will use a single premium immediate annuity-SPIA as the delivery system for the lifetime guarantee income however you can use a fixed index annuity with an income Rider as well, personally it doesn't matter to me as long as when you are selecting your lifetime guaranteed income source, you select the option that provides you the highest contractually guaranteed payout, if it's a SPIA great if it's an FIA great!

Assuming a $1,000,000 SPIA (As of June 2025), the joint lifetime income payout is $5,062.67 with a 17-year certain period.

I use a 17-year certain period to guarantee the entire starting balance will be paid to you or your beneficiaries. (The Insurance Company doesn't keep one dime of your money) Either you will spend it, your surviving spouse will spend it or your designated beneficiary will spend it!

If instead you select the Single Life with 13 1/2 year certain, the guaranteed lifetime income payout is $6,281.14 per month!

A difference of $1,218.47 per month / $14,621.64 per year! Over 30 years of retirement, close to half a million more in income... $438,649.20! After you account for the cost of maintaining both IUL insurance polices the increased lifetime guaranteed income would total $330,649.20!

This quote was based on a plain Jane SPIA but if an FIA pays a higher contractually guaranteed income (and 69% of the time it does) then the FIA will be used!

In this example, I used a male age 67 as the primary! Let's assume the husband dies at age 75, 8 years into the single life, guaranteed income!

The surviving spouse would continue to receive 5.5 more years of guaranteed income, plus the $500,000 death benefit!

The spouse is now 68 years old when the husband dies in this example.

The spouse will continue to receive $6,281.14 per month for 5 years and 6 months.

The spouse will put the $500,000 life insurance death benefit into a 5-year MYGA Annuity with zero fees, assuming a guaranteed rate of 5%!

Once the original annuity's certain period is finished paying the additional 5 years of income, the surviving spouse can now turn on a lifetime guaranteed income stream from the $500,000 death benefit, which was put into a 5-year MYGA earning 5% which is now $641,679.34

This would provide the surviving spouse with $4,310.39 per month guaranteed for life with a 12-year certain period and when the surviving spouse dies, the beneficiaries will receive a $500,000 death benefit from the 2nd life insurance policy. If the surviving spouse dies before the 12-period certain is up...the beneficiaries will receive both the $500,000 death benefit along with the remaining period certain income stream!

With the original Single life payout, two people shared $6,281.14 per month, or $3,140.57 each!

The income generated from the life insurance policy for the surviving spouse is $4,310.39, giving the surviving spouse an additional $1,169.82 per month compared with to the original income payout! Keep in mind...for 5 years and 6 months in this example, the spouse received an increase of The income generated from the life insurance policy for the surviving spouse is $4,310.39 giving the surviving spouse an additional $1,169.82 per month, compared with to the original income payout! Keep in mind...for 5 years and 6 months in this example, the spouse received an increase of $3,140.57 per month, an additional $207,271.02! (66 months)!

If the spouses' life expectancy was the full 12 years of the period certain, and you averaged out the remaining income with the first annuity payout, along with the income generated from the life insurance policy! This would be the equivalent of receiving $5,326.42 per month for 17 years!

Guess what!

I didn't have to use any fancy math, didn't have to worry about the cash value rate of return, didn't have to worry about the rising cost of insurance, don't have to worry about the life insurance premiums increasing and don't have to worry about the life insurance death benefit decreasing!

Recap:

I get it... Most agents or advisors using an IUL only use it for the cash value! I'm one of the few who doesn't (93% of the time)

Using an IUL not for cash value but setting the policy up with the ENLG rider -Extended No Lapse Guarantee Premium, you can....

1. Provide a death benefit in the event of death!

2. Provide a pool of money in the event of a major health concern such as having a heart attack, stroke or cancer...thus keeping you out of foreclosure or bankruptcy, keeping you from having to dip into your retirement nest egg!

3. Provide a pool of money to be used just in case you wake up one morning and you've lost the ability to bathe yourself or feed yourself or any of the 6 activities of daily living (LTC type services)

4. Provide a lever to increase your lifetime guaranteed income during the years you will spend the most amount of money, which is during the first 10 to 15 years of retirement!

The primary purpose of this report was to illustrate how using an IUL -Index Universal Life Insurance Policy set up with guaranteed premiums for the life of the policy by way of the ENLG -Extended No Lapse Guarantee Premiums!

An IUL with a dial to Extended No Lapse Guarantee Premium up to age 121 using living benefits with a dollar-for-dollar payout. This policy can literally save you thousands when compared to a traditional long-term care policy!

This report details how the "Gurus" get it wrong when speaking about cash value life insurance and the role it plays in your overall balanced financial plan!

Will this strategy work for everyone? NO!

Like all strategies, timing is everything!

The best time to purchase an IUL with guaranteed premiums is late 20s to early 30s. These strategies can work in your 50's but clearly the numbers are way more favorable if you plan ahead!

If you decide to implement this strategy, you must make sure to:

1. Use an IUL with an Extended No Lapse Guarantee Premium up to age 121

2. Use an IUL with living benefits using the "Dollar Per Dollar" formula

There's only a handful of IULs that combine both of these features.

Please reach out to my office for more details!

Book A Discovery Call

Long care, Planning doesn't start when you turn age 60! It starts Today! The sooner the better. Age 25 is the best age to get started.

With my planning approach I use a multipurpose policy.

It's a life insurance policy that can protect you from multiple life curveballs!

1. Income or inheritance for your family at time of death.

2. If you are in your 30s, 40s, 50s, and experience a major critical illness such as a Heart Attack, Stroke, or Cancer..... With this policy in place, you don't have to interrupt your compounding interest by dipping into your investment accounts.

Let your investment accounts continue to grow while this special life insurance policy provides you with cash on hand ($50,000 to $1,000,000) to deal with any extra expenses related to having your medical emergency!

a) Use this money to replace your income while recovering at home!

b) Use this money to continue making mortgage and car payments!

c) Use this money during retirement to pay for long term care type services!

d) Use the actual policy to help increase your lifetime guaranteed income!

Find out more today!